Financial Planning is one of the most important task that we should do, through out of life time. Most people give some thought to Financial Planning only when they think about Tax Planning. Most people tend to ignore one fact that, sometimes they can save/earn much by simply paying tax, and investing in some other instruments like Equities than a few tax saving instruments like Infrastructure Bonds. At the same time, you can save upto 30000/ just by cutting tax.

When it comes to Tax Saving instruments, there are a lots of schemes, like Public Provident Funds(PPF), National Savings Certificate(NSC), Infrastructure Bonds, life insurance, medical insurance, pension plans, Equity Linked Savings Scheme(ELSS) also called Tax Saving Mutual Funds, and a few more. All these have their own risk-return tradeoffs, lock-in periods, etc.

Investors often tend to ignore various nuances, decide the proportions artibrarily without much thought about the risk-return equation, investment objective and invest in a product for wrong reasons. Before you start tax planning, you should keep in mind that it is yet another investment you are making.

There is no difference between Financial Planning and Tax planning, except that in Tax Planning, you have a little lesser options than that is available for normal financial planning.

Before starting you planning, list out the various objectives of your investment. A few questions are as follows...

- You should be clear with the amount of risk, you are ready to take.

- The investment time frame.

- Your immediate financial liabilities. Like, you may need money for your sister/daughter's marriage, for your children's higher education, etc.

- When are you planning to retire? For most people it will be around 55-60 years. But a few people in software industry tend to retire as early as 50 years itself.

- Whether you will work continuously, or will give break for doing higher studies.

This is only a very limited set of questions. You should get your complete requirements.

At the end, most of these conditions becomes a function of your age. For example, younger people can take more risk, than people nearing their retirement, etc. Keep in mind, there is no single asset allocation proportion that fits all. But this is a high level idea, that you can consider while you do your tax plan.

Age less than 25 years:Probably you would have got a new job. Depending on the salary, you may not need to save upto 1lakh to zero your tax, or on the other extreme even if you invest 1lakh, you cannot zero your tax. I assume, you have to save full 1lakh and proceed, but you can change it proportionately. You are at the fourth stage of life as said in

William Shakespeare's

As You Like It where he speaks about

the seven ages of man. You are a brave soldier who is willing to take risk... Your investments at this age can contain some high risk instruments.

Life Insurance:You are young. You should not put your dependents at risk in your absence. This holds true even if you are married. You should first think about insurance. Insurance is a most important need at this age. Remember insurance is best bought at an younger age

Your parents may not have retired, so your income may not be the only source of income for them. So you can take some risky investments. The lure of taxation may not be the real reason for life insurance, but if you get tax benefits too, why do you hesitate?

Consult with an Insurance Consultant about the insurance amount and which plan to insure, and the time frame. But Life Insurance should form one of the large chunk in your investment.

Also in most of the schemes, you should pay a fixed amount through out the maturity date.

So, if you are planning to have break to do you higher studies, you should reconsider your investment in insurance.

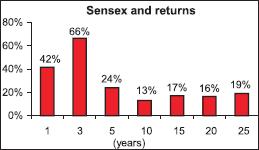

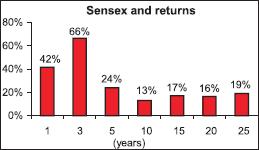

Equity Linked Savings Scheme(ELSS):You are young, probably unmarried. Your parents may not have retired. You have a long time on your side and being young you can take some amount of risk. So, you can invest some portion of your money in Equities, to boost your profits. There are a number of mutual funds available that avail tax benefits. The profit you make also is exempt from tax. But, these tax saving funds have a minimum lock-in period of 3 years. When compared to all other tax-saving instruments, ELSS has the minimum lock-in time. Also, ELSS has the capability to give a very high profit. But ELSS has the highest risk when compared to others. The very high risk involved is the compelling reason for the very short lock-in period. The returns from the Mutual Funds are tightly linked with the Stock Market. Although in stock market, you have a chance to lose your entire money in a short term, in the long term, stock markets have performed really well. Have a look at the Compounded Annual Growth Rate (CAGR) for the BSE sensex. This shows, even an investor who invests blindly on the BSE-30 stocks can expect an annual return of 15-20%, which is much more than the other fixed interest funds.

So, an intelligent fund manager with a lots of facilities for the latest information about the companies, and who can do good research about the various companies can provide a better return. Be cautious, your fund manager may even choose only the worst stocks resulting in loss too! But that will rarely happen. To rule out that worst case of choosing the worst fund manager who chooses the worst stock, invest in multiple funds, there by reducing the risk further.

Unit Linked Insurance Plans (ULIPs):ULIP is the mix of both the conventional insurance and mutual funds. ULIPs too has the same benefits as Insurance Plans with regards to Tax advantages. You can add this as a returns booster, if you have not invested in mutual funds already. ULIPs can also provide better returns over a long tenure. But keep in mind that the risk involved is much similar to the ELSS scheme, except that the Sum Assured is guaranteed, where as in Mutual Funds, nothing is guaranteed.

National Savings Certificate(NSC) and Public Provident Fund(PPF):

You may not invest these fixed interest savings, or invest a very less portion of the investment amount on these schemes, out of these two, prefer NSC over PPF. This is because, in NSC the interest rate is fixed when you invest and remains the same for the lock-in period(6 years), where as in PPF, the interest rate will be decided every year. With the interest rates dropping down steadily, you can safe with NSC than PPF. Also PPF has a continuous investment tenure of 15 years.

Age between 25-30 years:

If you got a job only in this tenure and previously unemployed, you can have a look at the previous section before looking at this section. For others this may help you.

Insurance:You are probably married and may also have kids. Now, your responsibilities in the family might have increased. You might have already insured. If not insure yourself against the unfortunate eventualities. You should not bet your spouse and kids on your demise. Also, revise the insured amount. You might have insured when your income was less, your income might have increased. Take help from your insurance advisor, and take additional insurance if necessary. Again, you can choose conventional insurance schemes or ULIPS.

ELSS/Mutual Funds:

You can reduce some of your investments from ELSS to reduce the risk. As your responsibility has increased and many more people depend on you, you can reduce some of your investments in ELSS and look for other low risk schemes. If the total risk you take is well within your risk appetite, you can have continue your investment in mutual funds.

Pension Plans:You are still young, but you can start early with your plan on retirement. If you are planning to retire from your job in 50's, this may be right time to start. If you plan to retire only at around 60 years, you can skip this step for a few years.

Since starting early can help you get a high pension amount. This is because of the power of compound interest.

You can consider either a conventional Pension Plan or Unit Linked Pension Plans (ULPPs). The ULPPs have a similar benefits and returns as the ULIPs. Have a look at the various terms and conditions on the scheme you invest, before you invest. Also, there are various options offered within the same pension plan scheme. To start with you may be aggressive, and latter switch to balanced and then with low risk investment options.

Assume an CAGR of 10%, calculate the amount accumulated at the end of 20 years and at the end of 30 years and compare, you will understand the difference. Say, you invest Rs10,000/ per annum. Then, you will have Rs18,10,000/ at the end of 30 years. Where as if you start after 10 years, and invest only for a period of 20 years and say you invest Rs20,000/ to compensate for the late start, you will have only Rs12,80,000/ That is you will get much lesser, inspite of the fact that you have invested double the amount every year. This is the power of compound interest, and the main reason for advising to start early.

Most financial advisors don't advice such an early start for pension plan, because they usually assume a retirement age of 58-60years, as in government institutions. Most IT professionals prefer to retire early, for them this is the right age to start.

NSC and PPF:

You can start investing on NSC and PPF a little, to reduce the risk. And prefer NSC over PPF because of the reasons quoted before. Make sure you keep only a smaller portion in these investments, because over a long time, NSC and PPF under perform other investment instruments.

Age between 30-45:You are stepping into the fifth stage (justice) as said by Shakespeare. You are neither too young nor too old. This the period with most responsibilities. You should take care of your old parents, you should take care of your children's education, save for their future, plan for your retirement, think about construction new house for your dependents, etc.

Insurance:

You would have already taken insurance, but the question is 'Are you adequately insured?' If not, take help from your financial advisor, to choose the right scheme. You can look at insurance plans with pension schemes too. At this age it is not necessary to look at pure risk insurance plans, but if you think you can pay only a lesser premium, you can opt for this pure risk insurance plans.

Pension Plans:

If you have not considered pension plan before, this is the time for you to start. Also, even if you have already planned for it, consider your present life style, and check whether the pension you are supposed to get, matches your present life style. You can also consider ULPPs, it is even better if you could invest some portion in ULPPs and some portion in conventional low risk plans.

ELSS/Mutual Funds:As you are not alarmingly old, you can have a little equity exposure, about 10-20% of your savings, depending on your risk profile, and age. That is around Rs10,000-Rs20,000/ will be good enough as a returns booster to increase the returns of your investments.

NSC and PPF:

My opinion on these options remain the same. Also prefer NSC over PPF. You can slightly increase the amount you invest on these.

Debt Funds:

Debt funds and liquid funds are one of the low risk, low return schemes. These doesn't have tax benefits. But these funds provide consistent returns, without any risk, better than the infrastructure bonds that have tax benefits. But try to allot as low amount as possible on such funds, since these funds have a very low return when compared to other investment instruments.

Age above 45 years:You are in the sixth stage of seven stages. You may not be too old, but this time you should consider more about your retirement. This is the age at which you should look for low risk investments. In this period, you will need money for you son's higher studies, you will need money for your daughter's marriage, you may need money for your medical expenses, etc. You should not risk your children's future, by investing on high risk instruments, after all, its for their future, we work hard to earn, he plan a lot to save money... So invest much lesser portion of your money in ELSS and equity related schemes.

Insurance:At this age if you feel you are not adequately insured, you should insure yourself. You can better look for pure risk only insurance plans, since these need lesser premium.

Pension Plans:

Never late than never, plan for your life after retirement - the seventh stage of your life. Your PPF account might get matured. You can invest that amount on Single Premium Pension Plans. At this age, avoid getting into ULPPs. The risk-return ratio of ULPPs may work against your own.

ELSS/Mutual Funds:

If you are not too close to retirement, you can invest a very less portion of your money on equities. You should invest only the money that you are ready to lose. So, you investment on these funds should be much lesser than 10% of your total investments.

NSC/PPF:Don't open a fresh account in PPF, unless you are not too close to retirement. If you already have PPF account, you can invest your money on the same account, so that the lock-in period is somewhat lesser than 10 years. You can get into NSC bonds, since it has a lock-in period of only 6 years, you can be safe investing in NSC. Also PPF and NSC has the lowest risk. This will suit you the best at this age, than any other.

Debt Funds:

Debt funds don't have tax benefits. But instead of investing in infrastructure bonds which has a low risk and a very low returns, you can better pay the tax and invest in debt funds. Debt funds also has less risk, but the returns are much better than infrastructure bonds.

Customize the plans to your needs:The various ways of investments that I have mentioned above are too generic. You should consider your responsibilities in your family, your economic and health conditions, etc. I haven't mentioned about taking house loans. Because house loans are not an instrument to save tax. It is only an additional benefit that you get if you take house loans. If you currently stay in a rented house, then take house loans, insure your house loans so that you don't risk your dependents' shelter on your loss. Most important fact that you should remember is financial planning is a continuous exercise. You should plan, change your investment strategy based on your changing life style, increase income, etc.

I hope this article will surely help you during your financial planning exercise. Your comments are welcome.

Happy Investing!